As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE firm clients. In our most recent installment, we discuss why leading PE firms are choosing to engage specialized executive search firms over larger generalist recruiting firms.

Learn more by watching the video below.

Interested in connecting with a specialized recruiter or any other type of third party? Contact us here. You can also learn more about the specific ways we drive value for PE firms by connecting them to the exact-fit resources they need by reading our case studies.

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE firm clients. In our most recent installment, one of our Managing Consultants, Scott Bellinger, talks about how leading PE firms are utilizing third parties to manage procurement issues that have been brought on due to inflation and supply chain issues roaring out of control.

Learn more about the unique ways in which PE firms are utilizing third-party procurement groups by watching the video below.

Interested in connecting with a third-party procurement group or any other type of third party? Contact us here. You can also learn more about the specific ways we drive value for PE firms by connecting them to the exact-fit resources they need by reading our case studies.

Every quarter our team analyzes the projects we work on with our 500+ PE firm clients to get a birdseye view of the market. You can request your copy here to view all of the trends that we have seen over the past quarter.

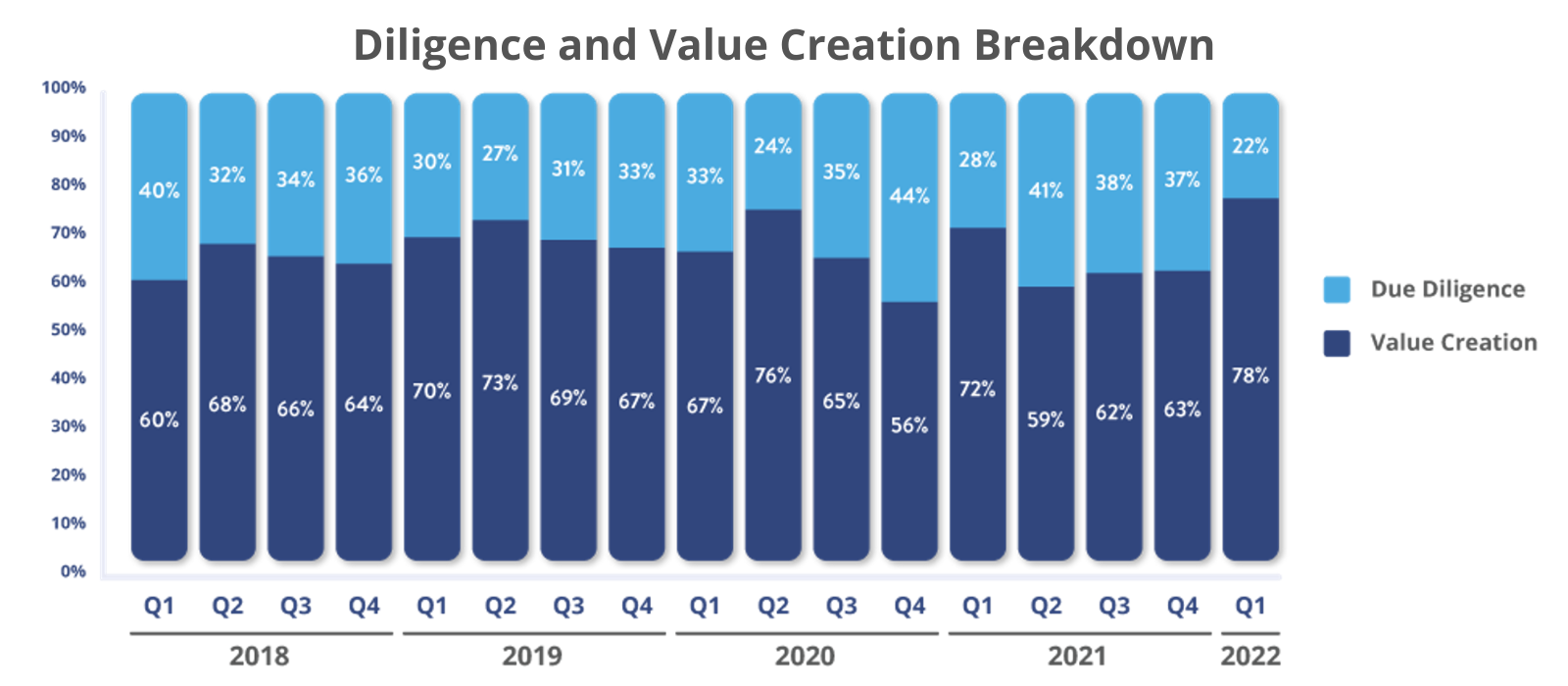

Key findings from Q1 included value creation at a historical high, deal flow reflecting 2019 versus 2021, & inflationary pressures impacting how firms thought about everything from pricing to talent.

Learn more about the insights we gleaned from the report by watching the video below.

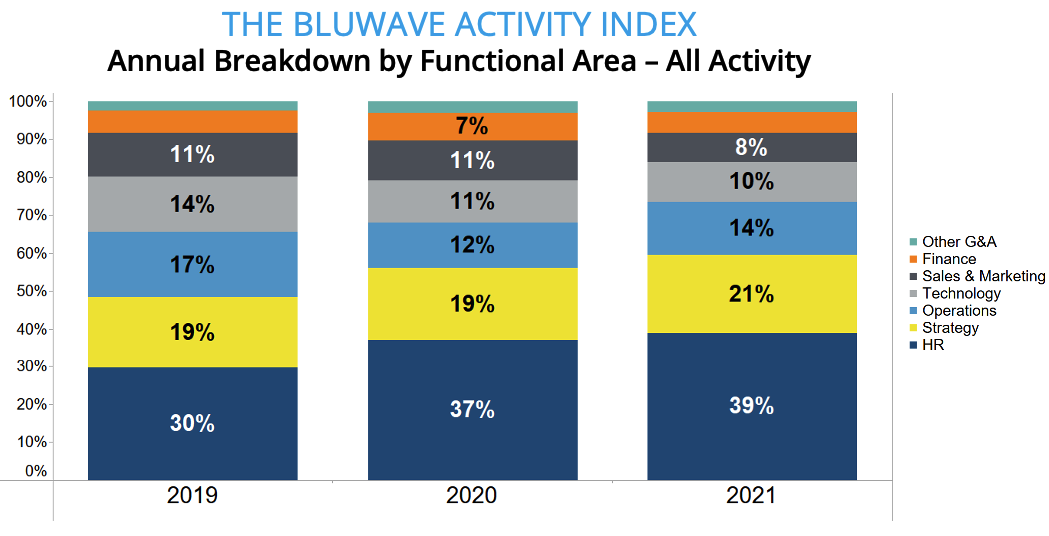

BluWave has a unique vantage in the private equity industry, working with more than 500 of the world’s top private equity firms across thousands of projects in due diligence, value creation, and preparing for sale. From this activity, we’re able to discern unique insights regarding how and why the world works. The top insight of the first quarter of 2022 relates to value creation. A staggering all-time high record 78% of initiatives tracked in the BluWave Activity Index related to value creation. Here are a few other trends that you might find helpful. Human capital is becoming increasingly important in private equity. With the fallout from The Great Resignation still alive and well, firms are struggling to fill key roles, which has resulted in an increase in time and resources invested in human capital. Across the BluWave Activity Index, 42% is related to human capital, which is up from 36% in the previous quarter. Firms have been utilizing specialized HR resources to recruit A-level talent, retain key players, and bring in critical interim skill sets. One of the biggest trends we’re seeing in private equity and the broader global economy is inflation. We’re seeing PE take proactive measures using specialized third-parties to help them pass through rising input costs, defend against price increases, and hone the operational efficiency of their portfolio companies. For more unique private equity insights, request the BluWave Q1 Insights Report today by following the link below or by contacting us at info@BluWave.net.

The COVID-19 pandemic accelerated our world’s digital transformation and has made businesses increasingly more virtual. In a tech-driven world, cybersecurity is vital to a business’ success, and it’s an area that is constantly evolving as the tech landscape shifts with new advancements. In fact, in 2021, we saw IT strategy land the number 6 spot in the BluWave Value Creation Index, signifying that cybersecurity was a top area of focus for PE firms, their portfolio companies, and proactive companies.

Staying up to date with the latest and greatest in cybersecurity is a full-time job that most companies don’t account for, causing many to fall short in digitally protecting their business. Thankfully, there are service providers out there that can take on this vital job for you and take care of your cybersecurity needs.

Curious what you may not be doing that you need to be? Trying to determine whether or not third-party cybersecurity expertise is something you need? Check out the PDF below to discover the 10 most common cybersecurity gaps companies face and how to avoid them.

If any of these gaps resonate with you, it may be time to connect with a third-party provider. We have a deep bench of PE-grade, pre-vetted service providers with specializations across various industries that we would be happy to connect you with – contact us here or use the “Start a Project Button” in the top banner.

Interested in learning more about how we can help with firms’ and companies’ digital and IT-related needs? Check out the below case studies:

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE firm clients. In our most recent installment, one of our Private Equity Consultants, Ryan Perkins, talks about the significant upswing COVID caused in the price of inputs. He shares two approaches companies can take in order to solve for this challenge, the negative impacts of each approach, and how BluWave can help in these scenarios.

Ryan gives an example of how we recently helped a high volume CPG business update their pricing across their product set, stay competitive with their eCommerce counterparts, and grow margins across their portfolio.

You can read another example of how we’ve helped a client with pricing strategy in this case study.

Learn more in the below video.

Do you need to get connected to a pricing analysis consultant or any other third-party resource? Be sure to click the “Start a Project” button above, or contact us here and we would be happy to get started in assisting you.

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE fund clients. In our most recent installment, our consulting manager, Scott Bellinger, talks about why we have seen an increase in go-to-market & growth strategy needs and how we are supporting clients with those. He shares that growth strategy is continuously increasing, with GTM being the third most used Value Creation use case in 2021, according to the BluWave Value Creation Index.

One of the most common ways we are helping clients with growth strategy needs is by connecting PE funds and their portfolio companies to senior advisors and consultants that can help them expand their reach outside of their current established market.

You can read another example of how we’ve helped a client with a go-to-market need in this case study.

Learn more in the below video.

Do you need to get connected to a GTM or growth strategy resource? Be sure to click the “Start a Project” button above, or contact us here and we would be happy to get started in assisting you.

Lean Six Sigma consultant need to improve operational efficiencies

A proactive manufacturing company came to us with a critical need for an operational performance and improvement consultant that could evaluate and redesign the existing layout of their warehouses. There was a lack of logistical reasoning that went into the original design and the company had recently discovered that the inefficiencies this caused were leading to foregone profits. The company immediately needed a Lean Six Sigma type consultant to come in and optimize the warehouse’s layout, process, and flow to increase operational efficiencies.

BluWave identified in network provider to meet niche needs

Leveraging our experience working with thousands of proactive companies, we have extensive frameworks for assessing operational performance and improvement needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of ops performance and improvement groups and independents that uniquely meet the highest standard. We interviewed the company to understand its specific vital criteria. We then connected them with two select, exact-fit, pre-vetted operational performance and improvement consultants from our invitation-only Intelligent Network.

The company engaged consultants to drive operational improvements

Within 24 hours of the initial scoping call, the company was introduced to two PE-grade ops performance and improvement consultants that specialized in optimizing efficiencies in small assembly-oriented manufacturing companies. The client selected their ideal choice and was able to confidently drive operational performance and improvement by increasing warehouse efficiency.

Cost-Reduction Group Needed for Leading Plastics Company

A leading plastics company that designed and manufactured innovative plastic-injection molded products was looking for opportunities to reduce their costs and believed potential opportunities lay within their legacy supply contracts. Given the nature of the company’s products and its specific resin grades, the company needed a group with deep expertise in this area to help them identify if this was a true area with room for improvement. The company asked us to connect them with a best-in-class cost-reduction group that has deep expertise in this industry with this specific need.

BluWave Assessed Company Needs To Identify Exact-Fit Provider

We first interviewed the company to understand the nuances of their needs and the unique challenges involved with post-transaction efforts to reduce costs. We then quickly matched these criteria to the pre-vetted candidates from our invitation-only marketplace, rooted in our experience working with thousands of proactive companies. Based on our proprietary approach, the company hired a group of resources with the exact plastics market experience they needed.

Client Engages Provider to Drive Success within Company

Thanks to the deep industry experience that the vetted group had as well as the key relationships that they had with needed manufacturers, the group of resources identified more than $10 million in annual savings for the client and created more than $80 million of pro forma enterprise value for the company.

Company needs specialized food and beverage executive recruiter

A proactive food & beverage company came to us with a vital need for a new VP of Operations after recently executing an add-on acquisition. They urgently needed an experienced food and beverage professional that could step in, take the reigns, and keep operations running smoothly while also implementing minor process changes that would be necessary while the two companies adjusted to the merger. In order to quickly fill this position with an exact-fit individual, the company was looking for a specialized food & beverage recruiting firm that had experience recruiting operations individuals for bakeries in the local area.

BluWave identifies niche recruiting firm with industry knowledge

Leveraging our experience working with thousands of proactive companies, we have extensive frameworks for assessing recruiting needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of recruiting firms that uniquely meet the highest standard. We interviewed the company to understand their specific key criteria, and then connected the client with the select pre-vetted recruiting firm from our invitation-only Intelligent Network that fit their exact needs.

Client engaged with pre-vetted firm to quickly begin hiring search

Within 48 hours of the initial scoping call, the PE firm and portfolio company were introduced to a PE-grade recruiting firm that specialized in recruiting executives for the food and beverage industry. The PE firm engaged with them and was able to confidently and quickly begin their VP of Operations search. The fund liked the recruiter so much that they also engaged them for their R&D Chef search.

Every quarter our team analyzes the projects we work on with our 500+ PE fund clients to get a birdseye view of the market. For Q4 of 2021, we not only pulled together our quarterly insights but also analyzed year-over-year trends dating back to 2019 to gain a deeper perspective (grab your copy here).

Key findings from our annual analysis included a sharp increase in the rise of human capital activity and rebounding of operational investment post-COVID.

Learn more about the insights we gleaned from the report by watching the video below.

An LMM PE firm ops partner and portco CFO came to us with a critical need for an IT Managed Services Provider (MSP) that could optimize and monitor the portco’s needs in the Azure development space. With past reliance on a small team that set everything up in Azure, their systems were in desperate need of optimization and 24/7 monitoring in order to ensure that no issues were occurring. They were in critical need of an MSP that had knowledge of the insurance business, was familiar with systems working for both internal and external users, and could understand how to use and integrate with APIs.

BluWave uses pre-vetted network to find top MSPs

Leveraging our founder’s 20 years in private equity, we have extensive frameworks for assessing PE-grade MSP needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of MSPs that uniquely meet the private equity standard. We interviewed the PE firm and portco leadership to understand their specific key criteria and then introduced them to two select pre-vetted MSPs from our invitation-only Intelligent Network that fit their exact needs.

Firm and portco confidently engage with ideal provider

Within 48 hours of the initial scoping call, the PE firm and portfolio company were introduced to two PE-grade MSPs that had the exact expertise they were looking for. As the decisionmaker for the project, the portco CFO selected their ideal choice. The portco was able to confidently engage the provider without wasting time or cost and rest assured that their services were running correctly thanks to the provider’s 24/7 monitoring.

Interim CFO needed for post-close accounting support at portco

A CFO at a PE-backed consumer products portco came to us with an urgent need for post-closing accounting support for an add-on acquisition the firm was about to close on for the portco. With the add-on about to close, there was an immediate need for an interim CFO that could translate the target’s accounting to align with GAAP, help with monthly closes, prep for audit, begin budgeting, and more. The portco CFO quickly needed an interim CFO for the new add-on that had small company experience, analytical skills, industry experience, and who was available to be onsite for the interim work.

BluWave quickly identifies exact-fit interim available to work

Leveraging our founder’s 20 years in private equity, we have extensive frameworks for assessing PE-grade interim CFO needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of interim CFOs that uniquely meet the private equity standard. We interviewed the portco CFO to understand their specific key criteria, and then connected the client with two select pre-vetted interim CFOs from our invitation-only Intelligent Network that fit their exact needs.

Client selects ideal candidate to ensure smooth transition with add-on

Within 24 hours of the initial scoping call, the portfolio company CFO was introduced to two PE-grade interim CFOs that specialized in helping companies close books when undergoing a PE add-on acquisition. The client selected their ideal choice. The portco CFO was able to confidently engage the interim resource without wasting time or cost and gain the extra pair of hands he needed to ensure the add-on went smoothly.