The COVID-19 pandemic accelerated our world’s digital transformation and has made businesses increasingly more virtual. In a tech-driven world, cybersecurity is vital to a business’ success, and it’s an area that is constantly evolving as the tech landscape shifts with new advancements. In fact, in 2021, we saw IT strategy land the number 6 spot in the BluWave Value Creation Index, signifying that cybersecurity was a top area of focus for PE firms, their portfolio companies, and proactive companies.

Staying up to date with the latest and greatest in cybersecurity is a full-time job that most companies don’t account for, causing many to fall short in digitally protecting their business. Thankfully, there are service providers out there that can take on this vital job for you and take care of your cybersecurity needs.

Curious what you may not be doing that you need to be? Trying to determine whether or not third-party cybersecurity expertise is something you need? Check out the PDF below to discover the 10 most common cybersecurity gaps companies face and how to avoid them.

If any of these gaps resonate with you, it may be time to connect with a third-party provider. We have a deep bench of PE-grade, pre-vetted service providers with specializations across various industries that we would be happy to connect you with – contact us here or use the “Start a Project Button” in the top banner.

Interested in learning more about how we can help with firms’ and companies’ digital and IT-related needs? Check out the below case studies:

Every quarter we gather leading women in PE to discuss current industry topics and to offer intelligent women the chance to gather, share information, and decompress with one another. In our most recent event, we gathered to discuss the trending topics of continuing 2021 trends, deal process pressures, and inflation. We have shared the themes we heard discussed across different areas below.

These forums are invite-only and follow Chatham House Rules, so listed below are high-level takeaways only. Are you a woman in private equity and interested in joining fellow leading PE professionals during our next Women in PE Forum? Register for our upcoming Women in PE Forums here.

Continuing 2021 Trends: Many 2021 trends will continue into 2022. Deal flow will remain high and multiples will remain high. Once interest rates are raised, public valuations should slow, which may stabilize private valuations, likely around Q4. With so much capital chasing deals right now, multiples may stay high through 2022.

Deal Process Pressures: Only put resources towards deals you have a conviction against. Zoom made it easier to attend management presentations, so there is more competition than ever before. It is essential to have some type of differentiation to make yourself competitive. As timelines are crunched, and providers are booked up, it’s also essential to line up diligence providers at the start of the deal.

Inflation: The vast majority of portfolio companies are struggling with inflation and supply chain disruption. Portfolio companies need to figure out how to pass the increased prices along to the customer or absorb the higher prices. It’s okay to “fire” customers – if margins are too thin, it may not be worth keeping some customers.

We thoroughly enjoyed getting to gather with other leading women in PE to discuss these trending topics. If we can be of help with any of the above, we’d be happy to quickly connect you to the exact-fit, PE-grade, third-party resources you need.

Interested in learning more about BluWave? Check out our Introduction to BluWave video to learn more about us and how we can help you. If you have an immediate need, contact us here or use the start a project button above – we’ll be happy to help you right away.

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE firm clients. In our most recent installment, one of our Private Equity Consultants, Ryan Perkins, talks about the significant upswing COVID caused in the price of inputs. He shares two approaches companies can take in order to solve for this challenge, the negative impacts of each approach, and how BluWave can help in these scenarios.

Ryan gives an example of how we recently helped a high volume CPG business update their pricing across their product set, stay competitive with their eCommerce counterparts, and grow margins across their portfolio.

You can read another example of how we’ve helped a client with pricing strategy in this case study.

Learn more in the below video.

Do you need to get connected to a pricing analysis consultant or any other third-party resource? Be sure to click the “Start a Project” button above, or contact us here and we would be happy to get started in assisting you.

2021 was a record-breaking year for private equity, with total deal value reaching $1.2 trillion according to Pitchbook, and it isn’t expected to slow down in 2022. With record amounts of dry powder in the market ($1.32 trillion as of September 2021), S&P Global states that the demand for deals is driving valuations up. Between the pressure to find the right deals in a market that is flooded with opportunity, and the high prices that have to be paid in order to win a deal, commercial due diligence is more important than ever in order to ensure funds are being spent wisely.

A process that was once reserved for large cap funds with extra capital to spend on assessing a company’s potential end market in order to determine the soundness of the investment, commercial due diligence is quickly becoming a necessary standard operating procedure for all proactive PE funds. With this evolution of who is utilizing commercial due diligence comes the evolution of how it’s performed– no longer is it an activity reserved for generalist consulting firms. Private equity firms have discovered that in order to drive alpha in a sea of beta, smaller, more specialized commercial due diligence providers can provide them with more unique insights quicker.

Going Deeper Faster

Any consultant can accomplish commercial due diligence’s goal of providing intelligence on a target’s total addressable market, prospects for growth, competitors, risks, and other vital information through initial industry research. But specialized consultants with pre-existing industry knowledge don’t have to waste their time scratching the surface trying to gain a sense for the industry. Instead, they can provide a heightened sense of value by using their base knowledge to dig deeper and therefore provide more in-depth insights in the same amount of time.

This is why it’s no surprise that over the past 3 years, commercial due diligence has remained the #1 Use Case in the BluWave Due Diligence Index. Firms have recognized the long-term value that lies in going outside of their normal providers to work with small shops and independent consultants that can provide deeper insights faster.

Providing a Head Start for Value Creation

Commercial due diligence isn’t just a process that helps PE funds make wise investments – it establishes a foundation for future growth. The average holding period for PE assets is five years, which is a sound reminder that funds are often interested in forging long-term relationships with the companies in their portfolio. This is why it’s essential for the commercial due diligence process to be more than a routine vetting exercise and a perfunctory look at a company’s market. It should help funds explore opportunities for growth and methods of adding value that can turn a company into something its leaders never imagined.

By providing deeper insights into the nuances of an industry and having experience within it, specialized commercial due diligence providers are uniquely equipped to identify various opportunities for a target’s growth. With multiples at a historic high, this head start on value creation initiatives ensures your team will be able to hit the ground running and provide quick returns on the investments.

Ensuring Available Capacity

In a market flush with M&A activity, we experienced deal surges in 2021 that led to provider scarcity, especially within the larger go-to commercial due diligence providers. A benefit of specialized commercial due diligence providers during these times is their more available bandwidth. Because they aren’t being run to with projects across 8 different industries, they have the capacity to take on the projects that fall directly within their sweet spot. Even when service provider constraints have strapped the market, BluWave has maintained a 100% fill rate with commercial due diligence requests.

Over the past year, we have seen many firms that have resorted to a smaller, more specialized provider in times of scarcity permanently switch their processes going forward to always using a specialized provider due to the valuable insights they gained. In times where other PE firms are struggling to get the insights they need on the timeline they need, equipping yourself with unique insights quickly will provide you with competitive edge.

Interested in seeing how we’ve helped PE firms by connecting them to the specialized commercial due diligence providers they need? Check out these case studies:

We’d be happy to get started on connecting you to the specialized commercial due diligence provider you need, just give us a shout or use the “Start a Project” button in the banner above.

Every quarter we bring together top PE HR and talent executives to discuss current industry topics and to offer talent leaders in private equity the chance to gather, share intel, and decompress with one another. In our most recent event, we discussed many topics and listed our top takeaways below.

These forums follow Chatham House Rules, so listed below are high-level takeaways only. Are you in private equity and interested in joining fellow leading PE professionals during our next Human Capital Forum? RSVP for our next event on May 4th.

Talent identification & recruitment:

As firms continue to struggle with portco executive talent identification & recruitment, firms are having particular success exploring non-traditional recruiting tactics in a supported way, i.e. hiring from non-PE backgrounds but providing support to skill-up the newcomers.

Firms are using the assessment process to understand what drives and motivates candidates and then leaning into these aspects to not only identify candidates’ strong points but to also sell the job prospect without having to lean 100% on compensation. Another tip we heard on successfully closing the deal was to provide candidates with transparency for what happens post-exit, such as having successful case studies ready to show the candidates where past execs moved after a sale.

Using data – firms are exploiting their CRM by skill-coding candidates and having them on-hand when perfect-fit roles open.

Timing is key and shortening recruiting cycles seems to be the most assured way to increase the hiring success rate. PE firms are recommending that portfolio companies implement applicant tracking systems to help standardize and streamline recruiting processes.

Assessment, onboarding, & setting executives up for success:

Clarity and coaching are key. Set expectations from the beginning by showing the good, the bad, and the ugly with the portco. Then, share how the firm will support the exec and what the firm expects from them.

Provide the exec with the tools needed to hit the ground running—internal resources, systems, supplements to their development points, etc. and then give them the space to do the job. If PE ownership requires another 40% of their time at the outset, consider external resources to do the upfront heavy lifting.

One participant recommended providing new hires with an internal company culture “river guide” to help them understand and navigate the unique cultures of a given company. This is particularly helpful for new CEOs who are tasked with being change agents.

Use transparency in showing portco executives their development path and opportunities.

Firms vary on the resources they rely on for training on organizational health, leadership development, and other skills. Many are (at least beginning) full talent reviews of exec teams of portcos and increasingly implementing this practice with internal PE fund talent.

Employee engagement surveys are critical to understanding cultural and organizational health over time. How to get it started? Find a partner who buys in, start with baby steps, and show measurable success.

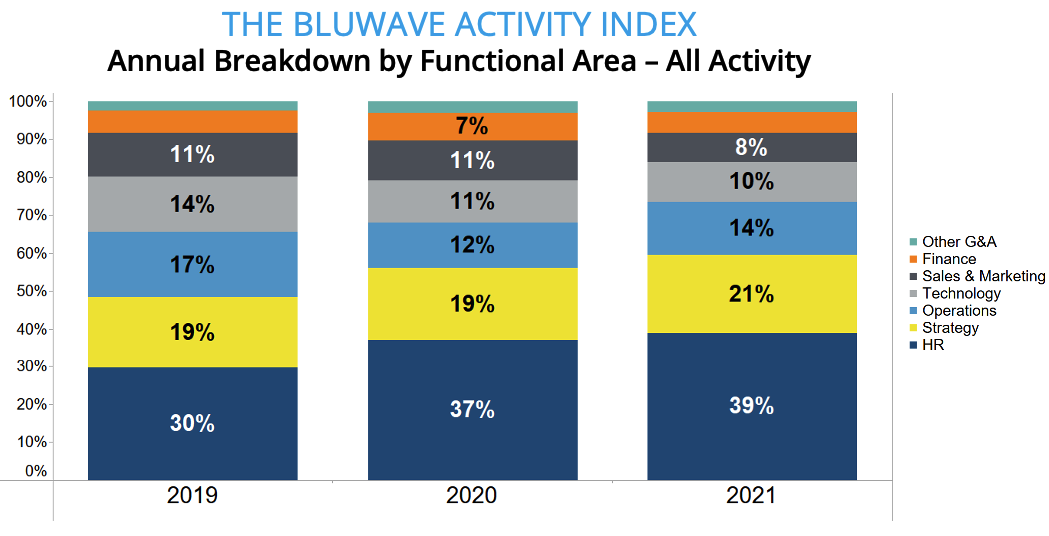

We thoroughly enjoyed the fruitful conversations that occurred during this recent gathering of PE human capital professionals. As noted in our 2021 Annual Insights Report, human capital remains one of the top initiatives in PE, with HR-related activities surging to 39% of all PE activity in 2021. If we can be of assistance during this busy time, please let us know.

Additionally, you may be interested in checking out some of our human capital specific resources, which can be found here:

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from our 500+ PE fund clients. In our most recent installment, our consulting manager, Scott Bellinger, talks about why we have seen an increase in go-to-market & growth strategy needs and how we are supporting clients with those. He shares that growth strategy is continuously increasing, with GTM being the third most used Value Creation use case in 2021, according to the BluWave Value Creation Index.

One of the most common ways we are helping clients with growth strategy needs is by connecting PE funds and their portfolio companies to senior advisors and consultants that can help them expand their reach outside of their current established market.

You can read another example of how we’ve helped a client with a go-to-market need in this case study.

Learn more in the below video.

Do you need to get connected to a GTM or growth strategy resource? Be sure to click the “Start a Project” button above, or contact us here and we would be happy to get started in assisting you.

BluWave works with over 500 PE funds from around the globe as well as their portfolio companies and proactive independent companies, connecting them with pre-vetted, best-in-class, third-party service providers across a variety of resource and functional areas. From information technology and manufacturing to healthcare, consumer goods, and beyond, our clients are expert business builders. In other words, they have their heads in the game and their hands on the pulse of news and insights you can use.

Check out the latest, curated collection of reports, insights, and musings from a handful of our PE fund clients on everything from community building across your portfolio, expected surprises for 2022, operational due diligence, and go-to-market strategies.

On the latest episode of The Private Equity Funcast, Jim, Cici, and Jimmy discuss their approach to building community within their portfolio. They share what has worked and what hasn’t for them, why community building is beneficial, and how they’ve seen their efforts have a positive impact across the companies within their portfolio.

Byron Wien and Joe Zidle share the unexpected, yet probable events that they think could shape the political, economic, and financial landscape in 2022. Some of the surprises they expect include persistent inflation becoming a dominant theme, group meetings and conventions returning to pre-pandemic levels by the end of the year, and ESG evolving beyond corporate policy statements including government-enforced regulatory standards.

Susan Clark, Managing Director and Head of Technology Value Creation at Sun Capital, joins several other private equity leaders on a Privcap Media podcast on best practices for operational due diligence ahead of PE investments. Susan shares what she looks for in ops diligence and how it helps create a go-forward plan post-close.

TCV’s Amol speaks with Trulioo’s CEO, Steve Munford, about how Trulioo’s customer base is integral to how they prioritize go-to-market channels on the Growth Journeys podcast. In addition to discussing GTM strategies, they also discuss tips and best practices for preserving culture across a rapidly growing multinational organization.

If you are in need of resources that can proactively help you with ESG, provide the specialized operational diligence you need, or help with your GTM and growth strategies, we can quickly connect you to the PE-grade, pre-vetted, exact-fit ones you need. Give us a shout.

Recently, BluWave founder & CEO, Sean Mooney, spoke with Gene Hammett on the Growth Think Tank podcast about what we at BluWave call the Karma School of Business. They discussed BluWave, what the first few years were like as Sean was growing the business, and the important leadership value of helping others be successful. Sean shares with Gene a practical example of how during COVID, we at BluWave saw a focus on helping others lead to dramatic growth. They also discuss other important leadership concepts, including knowing when to hire the right people and learning to let others take on responsibilities you have held in the past.

Interested in listening to the whole podcast yourself? Click below.

Every quarter we gather Operating Executives in PE to discuss current industry topics and to offer peers the chance to gather, share information, and decompress with one another. In our most recent event, we gathered to discuss lessons learned in 2021 that will be reinforced in 2022, creative ways to respond to the Great Resignation outside of paying portco teams significantly more, lessons learned from the seismic shift in traditional economy companies from field sales to inside sales approaches, and more.

These forums are invite-only and follow Chatham House Rules, so listed below are high-level takeaways only. Are you in private equity and interested in joining fellow Operating Executives during our next Operating Partners’ Forum? RSVP for the April 13th virtual forum.

Innovation from the COVID period and a return to basics: The COVID period has brought a focus on innovation in addition to a doubling down on the basics. Some of the fundamentals in making a company more valuable were sidelined over COVID due to many pressing and urgent pivots forced by the pandemic. Many operating partners are returning to the basics like pricing structure, automation, and expense management, as they can drive change faster and management teams are more open to listening. That said, the remote world continues to challenge relationships with portfolio companies and their management teams, and many ops teams are trying to solve for this by taking the opportunity to visit companies in person whenever they can safely do so.

Pervasive human capital issues due to wage inflation and scarcity: Nearly every participant expressed challenges related to turnover, recruiting, and wage inflation. These issues are complicated by the virtual or hybrid work postures of portfolio companies. PE firms are holding monthly portfolio-wide forums with key portco execs to share best practices. Portcos are doing things like town halls, stay interviews, and regular employee engagement surveys. PE firms are staying closer with portfolio management teams to ensure they have a handle on turnover, wages, and local comps. Culture continues to surpass most other factors in attracting and retaining key talent.

Moving from field sales to inside sales: Portcos with field sales teams are shifting to inside sales. Operating teams are helping equip these evolutions in a number of ways, including ensuring portcos have the right talent for the roles and bringing in expert advisors to help get the plan right the first time. Shifts to inside sales are being coupled with greater emphasis on account-based marketing, brand, content, and thought leadership via social media.

Digital transformation has been rapidly accelerated: After never quite gaining traction pre-COVID,digital transformation initiatives have been pulled forward by years.Popular digital transformation use cases included remote work, telemedicine, sales and marketing, and cloud migration. Digital transformation initiatives were previously justified based upon potential cost savings, but are now being made with customers and top-line growth in mind.

Analytics Taking Hold: COVID caused many to go deep into their data to inform strategies and tactics. PE firms are now building true analytics capabilities (including SQL, Python, and R know-how) internally and externally.

We thoroughly enjoyed getting to gather with PE Operating Executives to discuss these current hot topics and discuss how 2021 learnings will influence 2022 plans. If we can be of help placing interim executives, connecting you to a group that can help facilitate a digital transformation, or be of help with any other need, please contact us.

Interested in learning more about BluWave? Check out our Introduction to BluWave video to learn more about us and how we can help you.

Every quarter our team analyzes the projects we work on with our 500+ PE fund clients to get a birdseye view of the market. For Q4 of 2021, we not only pulled together our quarterly insights but also analyzed year-over-year trends dating back to 2019 to gain a deeper perspective (grab your copy here).

Key findings from our annual analysis included a sharp increase in the rise of human capital activity and rebounding of operational investment post-COVID.

Learn more about the insights we gleaned from the report by watching the video below.

Critical need for specialized recruiter for international hires

A PE firm VP came to us with a critical need for a specialized recruiter for their fintech portfolio company. As part of their growth strategy for the portco, they were gearing up to expand into more geographies, so they were in urgent need of language supports that could join their sales team. With expansion into the new markets happening later that year, the PE firm urgently needed a temporary recruiter that could hire 10-12 low-level sales individuals that had finance knowledge, fluency in foreign languages, and were located in the Chicago area.

Leveraging our founder’s 20 years in private equity, we have extensive frameworks for assessing PE-grade recruiting and staffing needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of recruiting and staffing firms that uniquely meet the private equity standard. We interviewed the PE firm to understand their specific key criteria and then connected the client with the select pre-vetted recruiting firm from our invitation-only Intelligent Network that fit their exact needs.

Engaging the recruiting firm, the portco successfully hires staff and expands internationally

Within 24 hours of the initial scoping call, the PE firm and portfolio company were introduced to a PE-grade recruiting firm that had extensive experience in recruiting sales individuals in the fintech industry. The PE firm was able to confidently engage the recruiter and ultimately successfully hire the individuals they needed in order to have full support as they expanded their geographic reach.

Charlie Gifford co-founded private equity firm New Heritage Capital in 2006, and has been investing in founder-owned, lower middle-market businesses for 22 years. He leads the firm’s origination practice, focusing his efforts on generating new investment opportunities and developing and maintaining intermediary relationships. In addition to his passion for the New England Patriots, Gifford is a strong believer in the concept of capital-and-thought partnerships for the companies in which his firm invests. The result: incentives for both founders and investors pointing in the same direction.

I caught up with him to get his take on everything from identifying the right-fit investments and what makes a great partner, to why expertise matters and the opportunities ahead for PE in 2022.

Sean Mooney: You co-founded New Heritage Capital in 2006, what was the genesis of founding the firm?

Charlie Gifford: I met my two current partners in 1999 while working for our predecessor firm. As that firm grew and began to move upmarket, the three of us were still interested in partnering with founder-owned businesses that had yet to access the institutional capital markets. Furthermore, we wanted to continue the model from our predecessor firm—one that incentivized all-star founders to stay on board for three to five years to help us grow the business. We wanted to be a capital partner and a thought partner to these founders. So, we essentially do an equity recap where the owner’s met their liquidity objectives, but we also allow the business owner to remain in control. Of course, the ultimate goal is to achieve superior returns for our investors, and we inherently believe the best way to do that is to identify bullish founders—owners who are interested in maintaining control post-close, and who are motivated by what we call “long term greed,” not just “short term greed.”

SM: You have a unique approach to investing called The Private IPO®—can you talk a bit about that, and how it’s differentiated from other forms of investment?

CG: I always like to point out that in the public markets you wouldn’t want to invest in a company where all the board members and executives are selling their shares. But in private equity, this is the standard model. A company gets acquired and as soon as a day later all the key executives can be laid off. This is counterintuitive to how great companies are built. We think it’s better when the founder is voting with their wallet and not their feet. In this way, we attract a self-selected cohort of maniacal owners who want to stay on board, want to remain in control, and are dedicated to growing their business.

In our Private IPO® solution, we provide significant up front liquidity for founders but also let them keep more control and earn a big piece of the upside. The founders we partner with come for the control piece, but they stay for the equity structure on the backend. If the business meets its growth targets, then they get a huge equity stake on the backend. As their partner, we help them to develop a growth strategy that allows them to double, triple, and even more in size, maximizing that backend equity value for everyone.

SM: What do you look for in a good investment, or partner? In other words, how do you identify founder-owned businesses that are the right fit for both New Heritage and the founder-owner?

CG: Interestingly, one of the very common traits we see in our partners is the individual that has worked at a large strategic competitor in their industry. They have grown a little skeptical about the prospects of growth: perhaps the company has taken their eye off the ball, isn’t innovating, or doesn’t treat the employees well. These founders have identified a clear market opportunity, so when they spin out of their current company they immediately begin to take market share by offering a better service or product. This new company is more nimble and meets the needs of their customer base more effectively.

SM: How do outside experts and advisors play a role in your business?

CG: If we look at the concept of market efficiency (where we are now versus 1999) there used to be no such thing as market networks. PE funds were left trying to figure out every detail out and conduct diligence on their own. The market is extremely competitive right now, particularly in terms of full-time talent; but the ability to call on BluWave for specialized project needs or interim executive talent means you have a better shot at not getting beat to the punch. In general, we are all attracted to growth, strong management, and industry tailwinds; but without the ability to get smart fast, it’s near impossible to be competitive.

SM: The pandemic certainly changed business as usual. What is the biggest lesson you’ve learned from the past two years? How has it affected your future outlook?

CG: One of the benefits of being a 15 person firm, many of whom have worked together for over a decade, is that there is a real comfort level in being candid, and a true sense of “all for one and one for all.” Everyone at the table has a voice. Our approach is collaborative and collegial. So, when the pandemic hit, we worked remotely for six months; but people wanted to come back to the office as soon as it was safe to do so. We inherently believe that this is an apprenticeship business and you learn by watching and doing. As for the future outlook, we think it’s bright. Our companies managed through COVID very well and the resiliency of the private markets has been incredible. We see strong earnings and strong deal flow in 2022.

SM: What are some major PE themes you’ve seen in 2021 that you think will have implications for next year (and possibly beyond)?

CG: For starters, PE will likely continue to pay up for good companies, and will be forced to close quicker with fewer contingencies. But I am just waiting for the music to stop, because things cannot go up and to the right forever. Having said that, it does say a lot about our country that our economy is still robust given all of these economic challenges created by the pandemic.

One common refrain we will continue to hear is the difficulty to attract workers and rising cost of labor. Due to this “missing middle”, prospecting and rainmaking has suffered somewhat, because everyone is working tirelessly on the necessary tasks to close deals in advance of year end.

SM: Now for the most important question: How do you really feel about Tom Brady leaving the Patriots?

CG: When you’re talking about the GOAT it’s hard not to wish him well, given the fact he always did what was in the team’s best interest by accepting a below-market contract. What he’s accomplished is truly remarkable. That said, I’m a Pats fan first and a Brady fan second, and now Belichick seems to be having the team playing it’s best football of the season around the holidays after a rough start– a true telltale sign of a Belichick coached team. It looks as though America’s worst nightmare is back…without Brady this time.