Company needs specialized food and beverage executive recruiter

A proactive food & beverage company came to us with a vital need for a new VP of Operations after recently executing an add-on acquisition. They urgently needed an experienced food and beverage professional that could step in, take the reigns, and keep operations running smoothly while also implementing minor process changes that would be necessary while the two companies adjusted to the merger. In order to quickly fill this position with an exact-fit individual, the company was looking for a specialized food & beverage recruiting firm that had experience recruiting operations individuals for bakeries in the local area.

BluWave identifies niche recruiting firm with industry knowledge

Leveraging our experience working with thousands of proactive companies, we have extensive frameworks for assessing recruiting needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of recruiting firms that uniquely meet the highest standard. We interviewed the company to understand their specific key criteria, and then connected the client with the select pre-vetted recruiting firm from our invitation-only Intelligent Network that fit their exact needs.

Client engaged with pre-vetted firm to quickly begin hiring search

Within 48 hours of the initial scoping call, the PE firm and portfolio company were introduced to a PE-grade recruiting firm that specialized in recruiting executives for the food and beverage industry. The PE firm engaged with them and was able to confidently and quickly begin their VP of Operations search. The fund liked the recruiter so much that they also engaged them for their R&D Chef search.

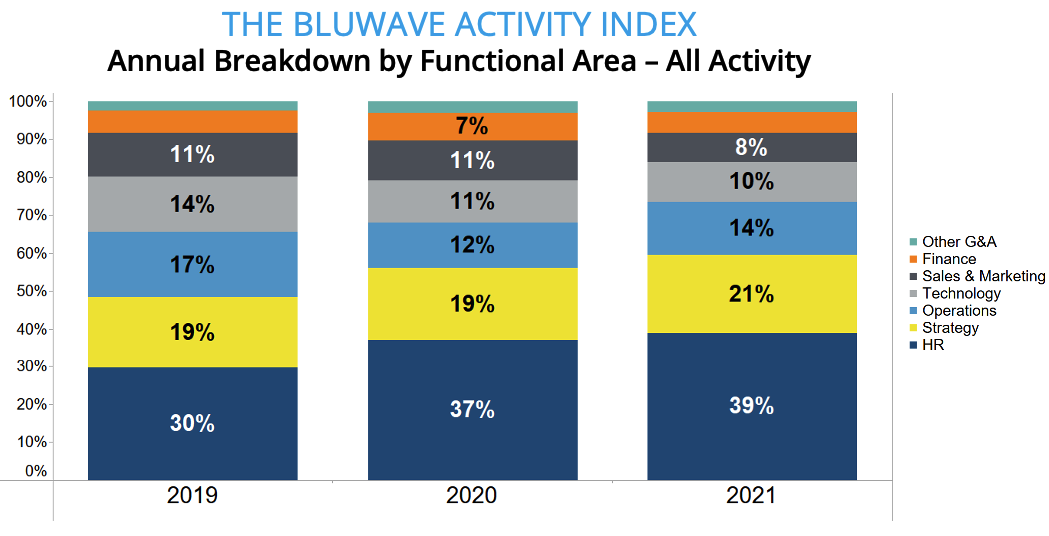

Every quarter our team analyzes the projects we work on with our 500+ PE fund clients to get a birdseye view of the market. For Q4 of 2021, we not only pulled together our quarterly insights but also analyzed year-over-year trends dating back to 2019 to gain a deeper perspective (grab your copy here).

Key findings from our annual analysis included a sharp increase in the rise of human capital activity and rebounding of operational investment post-COVID.

Learn more about the insights we gleaned from the report by watching the video below.

Russ Roberts is not your typical economist. As the longtime host of the podcast EconTalk, the John and Jean De Nault Research Fellow at Stanford University’s Hoover Institution, and a collection of economics-related books to his name, it would be easy to throw him into a traditional category. But, as the current President of Shalem University in Jerusalem recently told me: “My perspective on economics is constantly evolving as I learn more about what it is to be a human.”

Roberts also holds the title as a three-time teacher of the year and has taught at George Mason University, Washington University in St. Louis (where he was the founding director of what is now the Center for Experiential Learning), the University of Rochester, Stanford University, and the University of California, Los Angeles. He earned his Ph.D. from the University of Chicago and his undergraduate degree in economics from the University of North Carolina at Chapel Hill.

It is from this vantage point that I recently spoke with Roberts from his office in Israel about everything from his success as a podcast host and author, to his thoughts on the private equity industry, the construct of scarcity, and why expertise is necessary—but often challenging to vet.

Sean Mooney: How would you describe your brand of economics, and how has it evolved over the last decade?

Russ Roberts: I trained at the University of Chicago but became increasingly interested in the Austrian School—a heterodox school of economic thought. But I always found the most interesting questions were not about economics; rather they were more in the realm of philosophy, history, and social trends.

When I launched my podcast (EconTalk) I interviewed traditional economists on standard issues of economics– the trade deficit with China, bitcoin versus traditional currency, and the causes of the financial crisis. But over the years (and I started doing EconTalk in 2006), I got interested in other questions: Why are so many people in despair? What does it mean to be American? Why is there no longer a consensus about our national narrative as Americans? Why are tribalism and populism on the rise?

Economics is not the central tool kit for figuring out those questions. Many economists are often blind to non-economic factors: they look only at things that can be measured. But it can’t end there. The questions I ask are also questions of identity, role of community, and how to live with differences of opinion: the things that I believe are increasingly important.

SM: Why do you think that EconTalk has been so successful for so long? What’s your secret?

RR: Success is definitely hard to measure with something like a podcast. I’ve definitely learned a lot, and I get nice emails from listeners who are grateful. So, that certainly feels like success. On a personal level, as a 15-year long host, I have become a better listener and less of an “interrupter.” This is a wonderful life skill. And that means I give my guests, even those I disagree with, more of a chance to make their case and for me to engage with their viewpoint respectfully and civilly. I’m interested in conversations, not debate. This is a very powerful difference: conversation is about a shared exploration by two people, not just who’s right. When I created more room for my guests by doing more listening, I think EconTalk became a much better program. Lastly, I have learned to say “I don’t know.” It allows someone the opportunity to educate me—to let them be the expert.

SM: From your perspective, what is the biggest misconception about capitalism?

RR: Along the lines of what I alluded to above, the misconception people often have that wealth is a zero-sum gain—wealth must be taken from someone else. With just a little thought, you can realize that wealth is not a zero-sum game. Look at the standard of living today versus one hundred years ago: did we take the wealth from, Mars? Almost everyone got wealthier over time. Through technology, innovation, and processes, the standard of living has gotten better without making everyone worse off. Not at someone else’s expense.

Of course, there are always exceptions and bad players. The free market allows us to de-personalize the goods or services we are buying, and ultimately rewards the best X who is doing Y. We don’t have to like Jeff Bezos’ personal decisions, but we can still appreciate what he’s built and how it enhances our lives. One of the great gifts of a market economy is that you don’t have to peer into someone’s soul.

SM: We are living in a time of scarcity—in terms of the supply chain, the workforce, etc. How did we get here? When do you think this will shift and why?

RR: The concept of scarcity is an enormous challenge to economics and my way of thinking. I wrote ThePrice of Everything and It’s a Wonderful Loaf about the role that prices play in terms of order. Here is the quick take: Usually shortages are a sign of price controls, and usually when people say “we don’t have enough workers” it means that the price they have to pay is too high to get the workers. Historically, there have only been shortages when raising prices is forbidden. This happened with gas controls in the 1950s.

The puzzle with today’s shortages is why don’t suppliers just raise prices? My presumption is that they are afraid of being judged as gougers either by their customers or by the government. Eventually, prices will increase, instead of the other option: not having products. It’s already starting to happen. This will help eliminate the pressure on the supply chain.

SM: You are continually in conversation with experts in their field (for EconTalk): why do you think expertise is important?

RR: For the average citizen, expertise is in disarray right now. There is a lot of confusion about how to know whether someone is truly an expert—is it because they write books, host a podcast, make a lot of money, are on TV? It’s challenging to figure out the real versus the pseudo-expert, but we don’t want to fall prey to this postmodern phenomenon where people think everyone is a liar.

For a business, the challenge has always been the tension between making a decision that is defensible versus making a decision that is correct. If you’re an executive at a growing company, and you hire a first-rate consulting firm to help solve your problem, you can always make the defensible argument. But, if it turns out they can’t answer the question or find a solution, then what do you do? That being said, I think the challenge for business leaders is to feel confident taking a chance with a smaller, specialized, partner (without the big brand name) that is likely better equipped to tackle your problem.

SM: What is your definition of innovation? Where do we need more of it?

RR: Getting more from less, and achieving more with the same amount of resources. More simply put: we can make a process incrementally better, but what is even more desirable is making it better with the assistance of technology. A common example is the slide rule. Of course, we could make it incrementally better; but a calculator does a much better job with a fraction of the cost and much more accurately.

As a side note: I don’t think most people understand the pressure businesses are under to innovate, and why most founders don’t sleep well at night: they never know where competition is coming from. This is the essence of capitalism and what ultimately fuels growth and advancement.

In terms of the second part of the question, I think we need more innovation in the rules of the game: governance, how democracy works, etc. Antitrust law created for brick and mortar businesses is not helpful for thinking about big tech. In other words, we need innovative thinking about life as it exists in the digital realm, and how to evolve old systems in order to account for all of the changing dynamics.

SM: What is one piece of advice or knowledge you would share with those in leadership positions?

RR: Privilege your principles. If you want to make ethical decisions as a leader, and you’re worried about the existence of your business, it’s very tempting to do things that are not consistent with your principles. It’s always better to take an ego hit than violate your principles.

SM: Can you tell us anything about your next book?

RR: It’s called Wild Problems: A Guide To Making Decisions That Define Us. Generally speaking, I focus on the decisions we can’t necessarily measure or do a proper “cost-benefit analysis” about. Essentially, the book is an exploration of our sense of self, and how dignity and pride often outweigh the day-to-day effects of decisions we make. Today, we have so many choices and this leads to a lot of anxiety and stress. We want an app or data to help us make the best decisions, but that’s not the way everything works. If it was, life would be much more predictable, perhaps…but certainly less fun or interesting.

Pam Hendrickson is Vice Chair at the Riverside Company and a trailblazer in the world of finance and private equity. Growing up in Manhattan she was surrounded by the world of business. However, as a kid, opportunities in business also felt far away, as finance at the time was a landscape that was largely dominated by men. If you know Pam, she’s not someone who shies away from pursuing her dreams. She learned through determination, collaboration, and optimism that anything was possible. Pam studied hard, worked evened harder, and, after graduating from Duke, followed by a degree from Northwestern’s Kellogg School of Management, entered the world of finance in New York City. She joined JP Morgan Chase, ultimately rising to Managing Director during a highly accomplished career spanning over two decades with the firm.

As her career progressed, Pam was ready for the next challenge and wanted to more directly help companies build and grow. In 2006, she joined The Riverside Company as their COO. Once again, Pam thrived in one of the most intellectually stimulating and most challenging industries to succeed. Today, Pam serves as The Riverside Company’s Vice Chairman, where she supervises some fund strategies and monitors and manages policy, political, and legislative risk for Riverside and its portfolio companies. All along the way, Pam has paved a path for subsequent generations of diverse professionals in finance and private equity, enabling opportunities for others to succeed and thrive as she has.

She was kind enough to carve out some time for us recently, and the interview was revealing in so many ways: from her inside-look into Washington (and perhaps why politicians aren’t all bad) to her approach to diversity. In an industry that’s squarely focused on monetary returns, her insights are priceless. Our collective hats should tip to this powerhouse who uses her voice for those who are often kept out of the conversation.

Sean Mooney: As the current Vice Chair of AIC, what are a few of the core initiatives you are taking on in terms of lobbying efforts for the PE industry?

Pam Hendrickson: My focus is on helping make sure that members of Congress and the Administration understand private equity’s positive role in local communities across the country. Our industry employs over 11 million Americans, supports thousands of small businesses, and delivers strong pension returns for retirees. Fortunately, more people on the Hill now appreciate private equity and the tremendous value we add to the American economy.

I’m also working to explain the real-world consequences of some recent proposals in Congress that would change the tax treatment of carried interest capital gains. I’m especially interested in explaining how these proposals would harm the entrepreneurial ecosystem for women investors and entrepreneurs. The Ways and Means legislation would penalize investment firms by creating a potential tax penalty for adding new partners to existing investments. This would disproportionately expose women to nearly impossible barriers as they work to climb the corporate ladder at a time when firms are trying to advance diversity within their own leadership ranks.

Washington is trying to move very quickly: it’s like being in a baseball game but not knowing what inning you’re in. Oftentimes the intention of these proposals isn’t nefarious or ill-intended; rather, haste makes waste and politicians are drinking massive amounts of information from a firehose. One minute they are talking to someone like me, with a private equity agenda. The next minute, it’s someone from higher education, renewable energy, or critical infrastructure. Our job [as industry insiders and lobbyists] is to inform them about the realities and potential negative consequences in a non-incendiary way so they will actually listen; subsequently, we hope they make decisions based on the data-rich information we have provided.

SM: How would you define the Riverside culture, and how does this impact your investment strategy?

PH: At Riverside, our mantra is very simple, rooted in the golden rule: treat others the way you would want to be treated. This way of approaching investments, problem-solving, conversation, basically everything, puts the onus back on the fund managers to ensure we are making decisions that we would also make for ourselves.

Here’s an example of how this cultural value is operationalized vis-a-vis our portfolio companies: Some years ago, we made an investment in an educational company founded by a former teacher who saw a gap in the curriculum for kids, especially those on the autism spectrum. She created an entirely new language based on symbols not on letters—and this system has gained traction and been widely adopted in special education circles.

After the acquisition, her daughter took over the CEO position; she had never been a CEO, but she was familiar with the company, having helped get it through its initial growth phase. Instead of treating her like someone who needed “schooling” from us, we approached it from more of a consultative standpoint. This is how I prefer to be treated when tackling something new. No one likes to be patronized. Instead, our role was being more of a sounding board— she was especially happy to have her private equity partners during the early days of the pandemic because they could provide both advice and capital. Today, that company continues to thrive, and she has exceeded our expectations.

SM: Why does diversity at the highest levels of a company matter?

PH: My personal view is that diversity has more to do with various ways of thinking, experiences, and skills, rather than what someone looks like. How someone thinks about solving a problem has less to do with their gender or race, and more to do with their cultural attitudes and the background they bring to the table: education, where they grew up, how they managed challenges. A second-generation immigrant from Cuba who grew up in a single-parent household is going to have a different perspective than someone like me who grew up on Park Avenue in New York. This is a wonderful and necessary form of diversity—particularly if we have a shared interest in reaching a goal or outcome. What we miss with homogenous “group think” is likely why we’ve had recessions, wars, and insert any form of negative societal output. It’s just better business to have high-powered seats filled with versatile approaches to problem-solving.

How does this play out in the boardroom? We recently had an investment committee looking at a deal that sat squarely in the female products market segment. More than half of the people sitting at the table had never heard of this product and they didn’t understand what it did or why anyone would want it. So, they deferred to those of us in the room who understood the potential value of this product based on our experience—not simply on the numbers being presented on the slide deck.

SM: How has private equity changed over the last twenty years? If you were to sum it up in less than 10 words, what would you say?

PH: Funds used to make money on the buy. Not now.

The expanded version is: there used to be a time when multiples were low, and you could buy low and sell higher to generate great returns. Now companies are expensive to buy, so they have to grow quickly, and you can’t save your way to prosperity. This notion that PE “flips and strips” is just so far from the truth. Our whole objective is to get growth because we can’t increase value without top-line revenue going up and to the right.

SM: What is your hope for the future of PE? Where would you like to see it change, move, and transform?

PH: In general, one astonishing thing about PE is how little it has moved to technology. People in this industry still rely on Excel for tracking, measuring, and reporting. At Riverside, we have moved to upgraded technology because we are a volume shop, and we can’t afford to throw people at everything. But funds need to embrace technology. You’d think there would be more technology solutions that integrate, but they don’t.

For example: while there are some good systems for CRM, these don’t connect to a portfolio company’s reporting system that also needs to connect to how you report to LPs. It’s all fragmented and disjointed. All sorts of systems do financial reporting, but then the systems that show how you create value within the portfolio companies are entirely missing. As an industry, we need to move from manual processes to streamlined technology solutions. There’s an idea for an aspiring entrepreneur!

On a brighter note: I am delighted by the increased number of diverse owners of private equity funds. These investors will ensure access to capital to a broader and more diverse base of founders, thus attracting new, innovative companies into the mix.

SM: What keeps you going during the difficult moments when negativity abounds, circumstances look bleak, the world seems to be imploding. What’s your “secret?”

PH: I’m pretty lucky because I have a “high happiness” set point. When bad stuff happens, I just move on. I realize this isn’t the case for many, so I am very grateful to have been built like this—it likely is part of the reason I’ve been able to take so many risks and last in the investment world as long as I have. I remember in 7th grade the headmistress at my school saying something like: “You just happily bounce along. You need to have more angst about things, Pamela.” I remember thinking that was the most ridiculous thing I’d ever heard. I bounced off, and, from what I can tell, I was right to ignore her advice.

Within the first few minutes of my conversation with Matthew Garff, two things became crystal clear: He fundamentally believes in what’s possible and he approaches potential problems with radical honesty. This is a personal as well as professional attitude and has served him well throughout the course of his three decades career.

While the last two years have often felt like a mission impossible, Garff and the team at Sun Capital Partners (perhaps the name of the firm says it all?) remained a bright light for their portfolio companies, traversing uncharted territory and ultimately coming out ahead—mostly due to their investment strategy of focusing energy and resources on industries they know well, and a commitment to the people side of their founder and/or family-owned businesses. In his words: “Human capital is the most valuable asset in most companies, and people enable what’s possible. They are what ultimately make it successful.”

From working with founder-owned companies and prioritizing the Chief HR role to assessing acquisition targets through operational due diligence, in this interview, Garff reveals insights into how he thinks about the future of private equity and why that narrative needs a reboot. I couldn’t have said it better myself! Spoiler alert: although he spent several years of his career acquiring golf courses, his son is the real expert on the sport now.

Sean Mooney: Why is the due diligence process so vital to the acquisition or add-on process when assessing a company’s potential?

Matthew Garff: When we acquire a business, the company often needs help understanding what’s possible—far beyond what has already been accomplished. Generally speaking, with founder or family-owned businesses, they have had their heads down for a long time, grinding it out; so, when they engage with us our first objective is to try to uncover (or help management reach) the “possible.” The due diligence process allows us to understand where the business could be performing three to five years from now.

A good example is our portfolio company National Tree. It was a second-generation, family-owned business and a market leader in selling seasonal home decor through online marketplaces like Amazon and Wayfair. They had over a decade of experience working with these online marketplaces built a market leadership position in their niche products, which we learned through diligence would continue to grow. We also recognized their capabilities in sourcing and dropshipping products. With these core strengths, we saw an opportunity to leverage these skills and expand into tertiary markets, which National Tree is now doing.

As a result of our findings, and our roadmap for achieving what’s possible, in the last two years the company has experienced tremendous progress—they have added executive team members, instituted new operational systems and disciplines, and opened the door to add-on opportunities that will expand product categories and accelerate growth.

A nod to BluWave here: you helped us with FP&A resources that worked with us for several months after closing. This was an integral part of what we are now seeing in terms of National Tree’s expansion and continued market leadership.

SM: How is the process different when working with a founder- or family-owned business?

MG: I’d say the major difference is ensuring that there is a smooth transition from a cultural perspective. Typically, these founders and family owners are very attached to the business and even though they want to evolve and grow—which is why they partner with Sun Capital—they are seeing a lot of change happen to what they built, and that can be difficult. We collaborate with them on the “Shared Vision Plan” to ensure we are aligned in every way on the strategic direction and that they are on board with the changes.

SM: What are some of the obstacles the industry is facing?

MG: The industry is really healthy and the capital and know-how from PE is very constructive. However, too often I hear the pervading narrative that “PE is a destructive force in business through leveraging businesses.” The biggest obstacle we currently face is a negative perception of the industry, touted by those who have a public voice but choose to focus on the failed companies which were owned by private equity. The truth is, many private equity investments provide wealth creation for families, fuel innovation, and enable the economic growth engine.

I always say that these detractors offer a view of PE that’s akin to someone from another country visiting Los Angeles for the first time on the one day of the year when it actually rains. Then, they go back to their friends and say: “Ha! I knew it. Los Angeles isn’t sunny, it rains every day!”

SM: What are some of the factors driving the momentum in the industry?

MG: In general, buyers are now more specialized by industry, and this makes them more informed. At our firm, we adopted the “focused industry” approach many years ago, and as a result, we are more refined in our thinking and decisions. This is good for sellers because they can find an investor-partner who understands the nuances of their particular business and industry.

I’ll use National Tree again, to give a clear-cut example of how this specialized approach benefits both parties. Currently, I spend most of my time in consumer and digital commerce. When National Tree had a rough patch with Wayfair, I picked up the phone and called my relationship at Wayfair. Within days, the problem was solved. In short: specialization supports the momentum we are now seeing industry-wide.

SM: How do you think about human capital when it comes to acquiring and managing portfolio companies?

MG: I believe human capital is one of the most valuable assets of any successful company. End of story. Several years ago, we wanted to increase the attention our portfolio companies were giving to human capital. As a solution, we put in place a strategy to have our portfolio companies hire a Chief HR Officer—a role that drives strategic thinking, fundamental change through processes, and design efficiencies. This person’s role is to think strategically about the business, then marry that strategic thinking with decision-making around human capital. He or she understands long-term objectives and implements a hiring strategy to meet these objectives. It was a game-changer for our companies and enabled us to swiftly drive change and make money for the shareholders.

If we are considering a company for acquisition, one of the key components of “HR diligence” is seeing if they have this role filled. If they do, it signals they are proactive versus reactive. Unfortunately, most companies are extremely reactive, but we’ve come to understand that having a Chief HR Officer is a core part of the business strategy. It’s not always easy to fill this role, because HR is too often put in a reactive role. But the HR function needs to be elevated to someone who can ask questions like: “Is there a hiring strategy and plan for who we hire six months to a year from now.”

SM: Many companies are going through hiring and recruiting challenges. How is Sun Capital helping support your portcos to this end, and what are some of the suggested solutions?

MG: We have long understood that strong cultures lead to strong performance. As a regular practice, we conduct surveys at our companies and measure the results. This is the only way to improve on it. When we are looking at companies to buy, or even when we visit our portfolio companies, culture is a key focus because it can make the difference in terms of hiring and retaining top talent; and having the most capable, skilled employees leads to better performance.

As an example, I was visiting a prospective company a few weeks ago, and as we walked the warehouse the employees were eagerly coming up to our tour guide, a company executive. They were saying hello, high-fiving, and seeking his attention. It became immediately clear that the company had a strong culture, and when we did some more digging we found that turnover was low and profitability high. This strong, healthy culture we witnessed first-hand also translated to strong performance.

While recruiting is certainly more of a heavy lift right now, I always remind our portfolio company leaders that employees need to understand the vision, and they need to know everyone—including managers and executives—are rowing in the same direction. When an employee feels like “our mission statement is ‘X’ but no one seems to follow it” this undermines culture, and can have negative consequences (not to mention high costs).

As a slight aside, the founders and Co-CEOs of Sun Capital have developed our company culture around the concept of radical honesty. In short, having honest conversations and being encouraged to voice our opinions is a core part of our DNA. This means everyone, from every level of our organization, is given the opportunity to be heard.

SM: Are there any industries that are being overlooked by PE firms right now? If so, why do you think that is?

MG: Successful investors often exhibit the quality of being open-minded and avoiding the temptation of the crowd, because the crowd is not always correct. For example, at present “brick and mortar” businesses are viewed as unfavorable, and in some cases, this is deserved. But many retailers that have strong underlying businesses will stand the test of time.

We recently acquired a mattress retailer called Mancini’s Sleepworld. For the last few years, the conventional thinking has been that online mattress retailers like Casper would push traditional retailers out of business. As it turns out, the opposite has been true; Casper now has physical stores, because customers actually want to “try before they buy.” By the way, Mancini’s is doing great and we expect this trend to continue.

Sun Capital has been a successful early adopter in other industries that may seem out of favor. Fortunately, this has allowed us to exit at higher multiples than we entered in areas like HVAC, produce, and contract manufacturing. While we do spend ample time deliberating the merits of a business based on industry trends, we try to stay open-minded based on a variety of other factors and be aware of what we see happening at a personal, local, and community level.

SM: Given all your past investment focus on golf courses do you have a favorite?

MG: If I’m being radically honest (I knew that would come back to bite me), I’m not a good golfer, and I really don’t get on the course much anymore. However, my 16-year-old son is an avid golfer, so when he asks me to join I generally take him up on the offer—it’s often the only time I get to spend with him. We recently spent a day at Rancho Park in Westwood (Los Angeles, CA), and apparently, it has the most traffic of any golf course in America. I was obviously thrilled with so many onlookers, given my current trend of 120+ strokes.

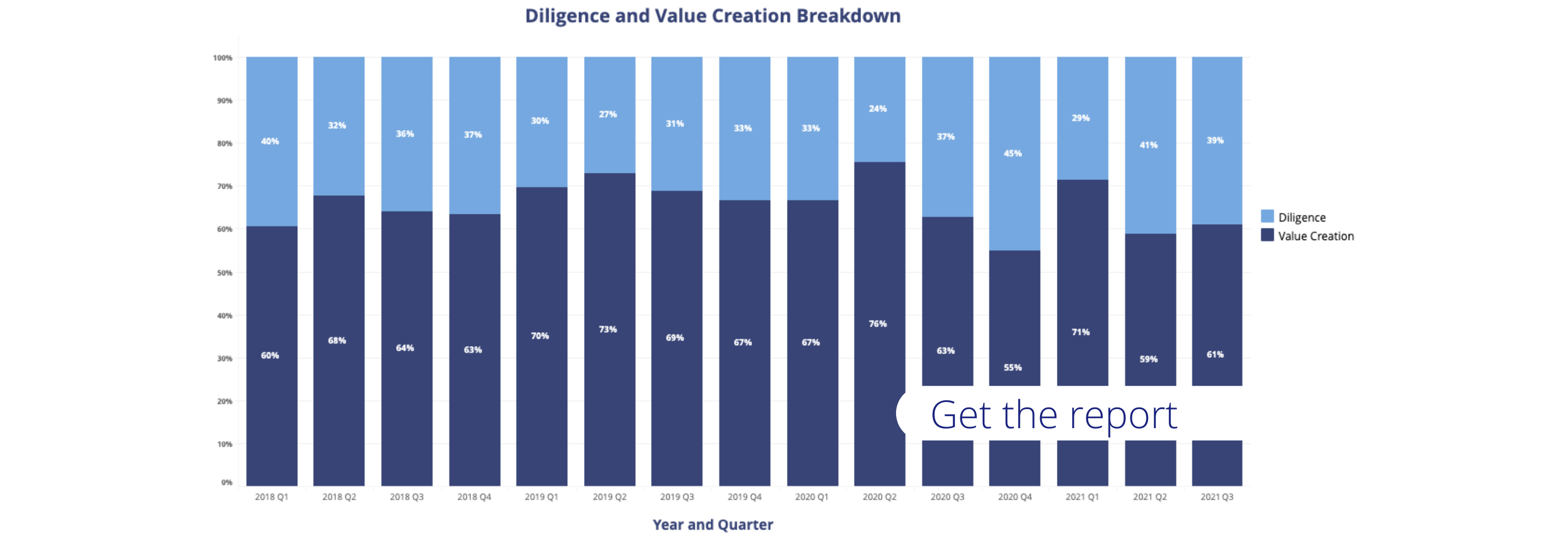

Every quarter our team analyzes the projects we work on with our 500+ PE fund clients to get a bird’s eye view of the market. This report (grab your copy here) calls out the trends that we are seeing across thousands of projects.

Key findings include deal surge continues – but due diligence is still a major area of focus, value creation is gaining momentum – one thing to specifically call out is that portfolio company operation performance and improvement had a huge spike in Q3.

To see these insights and more, watch the video below.

Arlington, Texas-based William Tincup is currently the President and Editor-at-Large of RecruitingDaily, one of the leading content publishers and conference organizers in the HR and “People” space. He stands firmly at the intersection of HR and technology and wears multiple hats as a seasoned writer, speaker, advisor, and consultant to hundreds of companies. His latest creative endeavor is hosting Recruiting Daily’s “Use Case” podcast, where he interviews executives from across various industries including our CEO, Sean Mooney and gets them talking about everything from launching companies and managing employees to their greatest successes and most profound failures.

To keep himself otherwise occupied and “feeling useful” (his words), Tincup serves on the Board of Advisors for companies like Clovers, MojoRank, Diversely, Skillset, Geescore, SturdyAI, Work4, and SmartRecruiters. He’s an active advisor and mentor with The Workplace Accelerator (Southeast Asia) ATK LABS (Israel) and Talent Tech Labs (New York City). In 2020, while the rest of us were trying to adjust to Zoom fatigue and mask mandates, he was actively advising three acquired companies: Altru, sold to iCIMS Q4 2020; Talentegy, sold to Jobvite Q3 2020; and Hyphen, sold to Betterworks Q1 2020. Let’s not forget he was also a board member of Talentegy, a company sold to Jobvite Q3 2020.

Suppose that doesn’t send your head spinning and also wondering what this Texan is eating for breakfast. In that case, rest-assured Tincup is less concerned with tooting his own horn and more focused on helping HR and talent acquisition (TA) professionals navigate uncharted waters—particularly in the wake of the pandemic and shifting cultural tides. His knowledge of everything from what candidates want from jobs to the importance of interim executives is worth listening to, if not ripping out several pages from his book.

Kyle Johnson: Tell me about your journey to RecruitingDaily.

William Tincup: I fell in love with HR while in business school, specializing in marketing. My first entrepreneurial endeavor was a web development agency; I later co-founded a full-service advertising agency. While at the ad agency (then called Starr Tincup, now The Starr Conspiracy), we specialized in helping vendors and service providers market to HR & TA specialists. Essentially, we learned what worked and didn’t work when marketing to these practitioners. While doing so, I was the partner in charge of everything HR & TA for the agency. The deeper I got into it, the more I fell in love with the profession. In 2010, I was lucky enough to sell my equity to my business partner, and then I shifted my focus to HR & TA full time.

I started by consulting vendors and practitioners in change management and user adoption of HR & TA software. I did that for a few years and loved it—I worked equally for both vendors and practitioners, solving real problems. Then, I decided to dig deeper into primary market research to learn more about implementations, user adoption, and vendor selection. After learning so much from the folks in the trenches and further expanding my knowledge base, I joined the team at RecruitingDaily to build the events and training business. In my current role, I get to talk with vendors and practitioners every single day. It’s incredible because I continually gain insights into where they see the world similarly and differently.

KJ: What is the number one thing you see people searching for right now regarding types of jobs and work?

WT: In short, “something new.” More specifically, candidates who were fortunate enough to be employed during the pandemic but unfortunate enough to deal with the constant disruption and stress are now coming up for air and looking around for new adventures. In tandem with this “fancy shiny object” job search, most candidates learned that much of their knowledge and skills could be effectively managed remotely. That’s a game-changer. Once people figured out they could live in Park City, Utah while working for a company based in New York City, many of them made substantial lifestyle changes to strike that elusive life balance. It almost gave people permission to shed old norms and start fresh. They went from thinking, “I’m going to be stuck in an office for the rest of my life,” to “holy cow, I can work on the ski slopes!”

Data certainly supports this new mindset: candidates are searching Indeed, Hired, ZipRecruiter, and company career pages using the words “remote” and “remote work.” They aren’t wasting time applying to jobs that don’t support their new ideal career. My take on this is simple: organizations that support remote work and its flexibility will win over those who choose not to. Talented people are going to work the way they want to work.

KJ: Talk a bit about Critical versus Important talent and the implications of both in getting the right talent in place?

WT: HR & TA has historically looked at talent through the lens of 80/20, meaning 80% of the value of any given organization is derived from 20% of the workforce. That would be essentially the “critical” talent. Important would be everyone else. When I interact with investors, they tend to use the lens of 90/10, which is an even harsher way to think of critical talent versus important (or necessary) talent. Again, this is a historical view of talent. This has been the way we’ve viewed succession planning, training for high potentials, executive search, and more.

I think we’ve got to update our worldview when it comes to talent; not only do we need to focus more on skills, but skills needed at that particular time. Just as manufacturers look at “just in time” production, we need to think about talent from that perspective. What skills do we need right now, this moment, this hour, and this week, for this project? It becomes less of a game of what you’ve done in the past and how relevant your skills are right now. Genuinely talented people will always push themselves to acquire new and most relevant skills. So, some of the same people will be on the list as if nothing changed from the history lesson above, but other folks that didn’t have a certain pedigree, skill color, gender, etc. but DO HAVE the critical skills needed will find themselves on the list. Having scarce and vital skills is now how you separate yourself from everyone else.

KJ: From your vantage point, what keeps HR up at night?

WT: It comes down to three things: (1) what is/isn’t “hybrid” and how do they do work, (2) how do they effectively attract talent, and (3) how do they effectively retain talent? Let’s unpack each of those:

#1—No HR leader knows how the hybrid workforce will look in the future. It’s all guesswork at this point. COVID forced us to rethink the workplace. We were already tracking towards remote work; the pandemic expedited the process. With other variants likely to come, no one knows when a safe return to the office will happen or if it will happen. This leads me to the next exciting aspect of hybrid work: the emerging concept of “everyone returns to the office” versus “I want to work remotely forever,” which are purposely opposites, but that’s what HR is dealing with right now and in the near future. How do they effectively navigate “radical flexibility” with all talent? Talent will ultimately decide where and how they work in an outcomes-based environment (read: knowledge working jobs).

#2—Talent attraction, acquisition, and recruiting have become more challenging as the talent is now empowered to ask tougher questions. The table stakes have changed. Let’s say you have a great culture. Well, that’s fantastic; but how did your firm respond during COVID? Did you furlough or lay off anyone? If so, have they been hired back? If not, why and what kind of package did you give them to get through the pandemic? That is a primary candidate question thread. Then comes the more complex stuff with questions about DIBEE (diversity, inclusion, belonging, equity, equality), social justice, remote work, and transparency, to list a few. So, the job of a great recruiter got harder. Don’t cry for Argentina; the best TA pros are highly compensated and in short supply. That just made things interesting. Hiring a TA leader pre-COVID was not impossible—indeed, not as hard as placing a data scientist or software engineer, but it’s getting real close to impossible at this point. Candidates’ needs have changed, as I’ve already noted. Recruiters’ needs have also changed. Companies that recognize this will work hard to retain the best recruiters.

#3—With retention, there are NO RULES. Do whatever you must to keep talented people. Whatever it takes. Turnover isn’t a curse word. Trees die in any given forest every single day. What you and your team should be focused on is “regrettable turnover.” Regrettable, meaning talent you wanted to keep but were unable to keep for whatever reason. How do you stop the bleeding of regrettable turnover? A few helpful hints: communicate that you value them, recognize the value they bring to the organization, find out what’s important to them and do your best to fulfill it, compensate them above market, conduct monthly stay interviews, and offer them continuous training. You get it. Do whatever it takes to learn what drives them, and then do whatever it takes to keep them engaged. No one wants to talk about it, but this is singularly the most essential thing HR does for a firm. Retention of top talent is the job. Get great at it quickly!

KJ: Why do you think interim talent and experts are such a vital component of the workforce right now?

WT: A few things to consider here, (1) expertise is earned, (2) it turns out B12 is a good idea. Let’s explore…

Throughout one’s career, we gather all kinds of experiences. Good, bad, historical successes and failures, and we should tap folks that have been there and done that. It doesn’t mean that we’ll do it exactly the way they have, but it could help us avoid simple mistakes. For instance, an HR leader that’s been a part of 20 union contract negotiations would be great to have at the table as we navigate a new deal with our union workers. That person can give us insight into things we don’t know and learn fast enough to impact the new contract. So, experts are vital. Early in my career, I was advised by a highly successful oilman in Dallas. I asked him over coffee, “what was the key to your success?” He responded, “simple, I let experts be experts.” Simple advice, but you’d be amazed at how many executives hire experts and summarily disregard their advice. Kidding not kidding.

That might not be immediately recognizable in terms of the B12 reference, but interim talent is like a shot of B12. If you’ve ever had a shot of this stuff, you almost immediately feel better. Interim talent is a lot like that—new eyes on old problems. A new set of eyes can see things that might even be obvious, but the previous folks didn’t reconcile for whatever reason. Interim talent also doesn’t necessarily have to play by the same rules nor play politics. They’ve been hired to an interim capacity to fix things. If you’re a Pulp Fiction fan, Mr. Wolf is an excellent example of interim leadership. All the other guys could have probably figured out what to do, but Mr. Wolf had been there and done that. He had a plan and communicated effectively. Problem fixed. Interim talent is an excellent way to invigorate or reinvigorate a team and organization like a shot of B12.

KJ: What question should I have asked you but didn’t?

WT: Well, you asked great questions, but I think I’d be remiss if I didn’t mention the recent decision by the SEC to include workforce data in publicly traded companies’ earnings calls. It’s new but has been in the works for over a decade. It will be weird at first, but I see it as an excellent opportunity for HR & TA leaders. If our house isn’t in order, now is a great time to get it in order. It’s pretty simple when the SEC says something is noteworthy, Wall Street listens. What happens on Wall Street eventually makes it to Main Street. So, if you’re not studying the new regulations, you might want to burn some hours learning what is required to be reported. I mention this not to scare anyone; think about the tremendous opportunity that’s been granted to those responsible for talent.

In a recent article for CEOWorld Magazine, BluWave founder and CEO Sean Mooney shared how his love for the beautiful, streamlined, and seemingly perfect Ferrari sports cars that constantly improved with each model led to his love for the concept of Lean Six Sigma. He saw a similar sense of beauty in the ideas of perfecting form, reducing variability, eliminating waste, and continuously seeking improvement.

While the concept was first embraced by the manufacturing industry, it is becoming increasingly popular across all sectors and industries, even in how business leaders think about their people.

You can read the full article and Sean’s thoughts on how Lean Six Sigma is all about people here. And if you need help connecting to the fractional and interim resources you need when you need them in order to apply Lean Six Sigma in your business, you can contact us here.

Every quarter our team analyzes the projects we work on with our 500+ PE fund clients to get a bird’s eye view of the market. In this video, our leadership team shares the trends we are seeing across due diligence and value creation. Watch the video below to learn more.

If you would like to get a copy of the report, reach out directly to your BluWave contact or our team at insights@bluewave.net and we’ll be happy to assist.

As the chaos and uncertainty around the pandemic starts to settle and businesses dust off the debris of the last year, it’s becoming clear that a new world of work is upon us. What many were predicting would soon be the “new normal” is now the actual normal—especially when it comes to work. The transition back into physical office spaces does not mean the end of remote work. Instead, companies are embracing a hybrid workforce.

Hybrid work combines virtual and onsite employees, whether on alternating days or on a permanent basis, and is a trend that companies are embracing across the country. A recent report from Gartner revealed that 59 percent of companies intend employees to work remotely occasionally, while 32 percent are allowing remote work full-time. For many leaders, however, this now means transitioning again into a new working style: one that facilitates productivity and collaboration among in-office and virtual workers (think: all-hands meetings with half the team sitting together at a conference table and the other half calling in from Zoom).

This is why project-based work is on the rise. Instead of onboarding full-time employees remotely, which has been one of the biggest challenges for HR leaders during the pandemic, companies are calling on skilled experts to complete tasks on a contractual, as-needed basis. As we drive ahead in the new normal, project-based workers will be fueling the future of work.

Project-based work is an integral part of a successful remote workforce

Across the 1,000-plus private-equity-based projects BluWave supported in the last 12 months, one thing stood out: investments in people continue to be the number one focus area in 2021. While technology has helped companies to adapt to remote work, hiring employees who have the skills to work with the technology has been even more valuable.

Hiring workers for specific, often discrete, projects means you can vet candidates based on their ability to meet the demands of that project. Using an Intelligent Talent Network can help you match potential interim workers to those interim needs. This model works well for private equity firms, from senior partners to portfolio company executives, because it engenders trust and rewards results. If you hire people who are skilled, action-oriented, and self-motivated, you can set goals and give them “rope” to freely deliver the best result. Ultimately, project-based work ensures that rewards are aligned and incentives are rewarded in exchange for top performance, which is more difficult to achieve with a more amorphous scope.

Interim work means more equitable environments

Hiring based on a potential employee’s ability to perform against predetermined, outcomes-based objectives helps eliminate bias (unconscious or not) in the recruitment process. According to Harvard Business School, “In recruiting … unconscious bias and affinity bias often express themselves as a preference for one candidate or another because of ‘culture fit.’ Resumes may be selected because of a shared alma mater, or because of an unconscious bias to one name over another.”

When hiring for a long-term fit, companies may choose to give preference to candidates who meet unspoken criteria off-paper—because culture-fit and soft skills are generally more relevant for full-time employees. With project-based work, it’s the results that matter. If someone has a track record of success, they meet the criteria. It’s that simple. Plus, in this system, rewards are made equitable, too. If your project scope is clear, you can offer fair and just compensation for the work that is done—it provides equality of opportunity to perform.

Creating collaborative environments with distributed workers

The key to effectively utilizing project-based workers is putting the right systems in place to seamlessly integrate them into the existing processes and work efficiently across project stakeholders for the duration of their contract.

Clearly defining and communicating goals from the onset, delineating established deadlines, and integrating collaboration tools into operations will help leaders stay on top of a project. These are hallmarks of agile development, which involves short, project-to-project scrums with siloed teams that collaborate consistently through the scrum. Research has shown that agile teams are 25 percent more productive than their industry peers because team members focused on one task at a time.

You can also implement clear structures for assigning roles and accountabilities. A RACI chart is a tried-and-true matrix used to assign roles on a project. A properly used RACI outlines who is responsible for executing tasks, who is accountable for the work, who is consulted throughout the project, and who is informed on project progress. This helps eliminate confusion, reduce duplication or redundancy, and ensure those deadlines are met.

For a workforce still in flux, those equipped for project-based work act as connective tissue and can build the foundation for future stability. Companies that embrace this wave of “normal” will likely be the ones that ultimately find themselves in a winning position.

A PE firm came to us with a critical need for a pricing strategy expert to maximize revenue at one of their consumer products portfolio companies. Since competing against big-box retailers, the portco realized their need to set pricing that clearly conveyed the value of their offerings to their price-conscious and value-driven consumers. We quickly worked to understand the client’s nuanced needs, leading us to promptly introduce them to two PE-grade pricing strategy experts with extensive experience in the consumer products industry. The client selected their ideal choice, and the PE fund was able to achieve its objective of maximizing response rates and demand through strategic pricing and an aggressive seasonal promotional schedule.

Do you have a similar need or any other specific need we can help you with? Contact us here and we will be happy to help you.

A private equity firm principal and portfolio company CEO came to us with a need for a Head of Sales for their healthcare logistics company. Since the acquisition, the portfolio company had been growing rapidly, and they needed to make key hires across multiple functions. Moving quickly, we worked to thoroughly understand the client’s specific needs. We introduced them to two sales recruiting firms that specialized in senior go-to-market roles in the healthcare space. After a thorough vetting process, the CEO made a decision and hired one of the candidates presented. To date, the partnership is a success and going smoothly.

Do you have a similar need in the interim exec area or any other unique need we can help with? Contact us here and we will be happy to help.